How much CPF savings can I withdraw from age 55?

This article answers the three most common questions about CPF withdrawal from age 55.

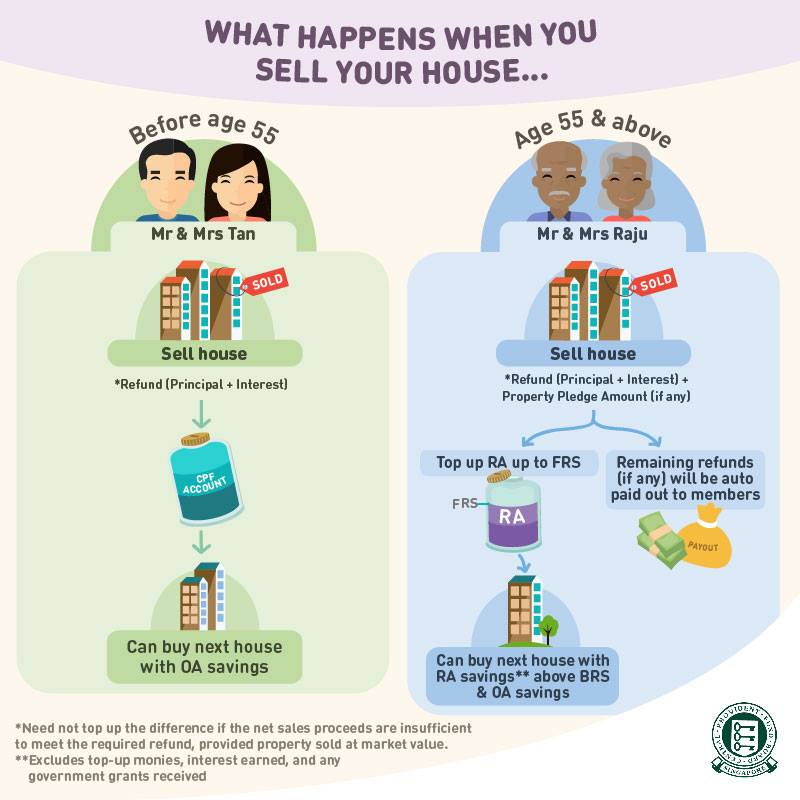

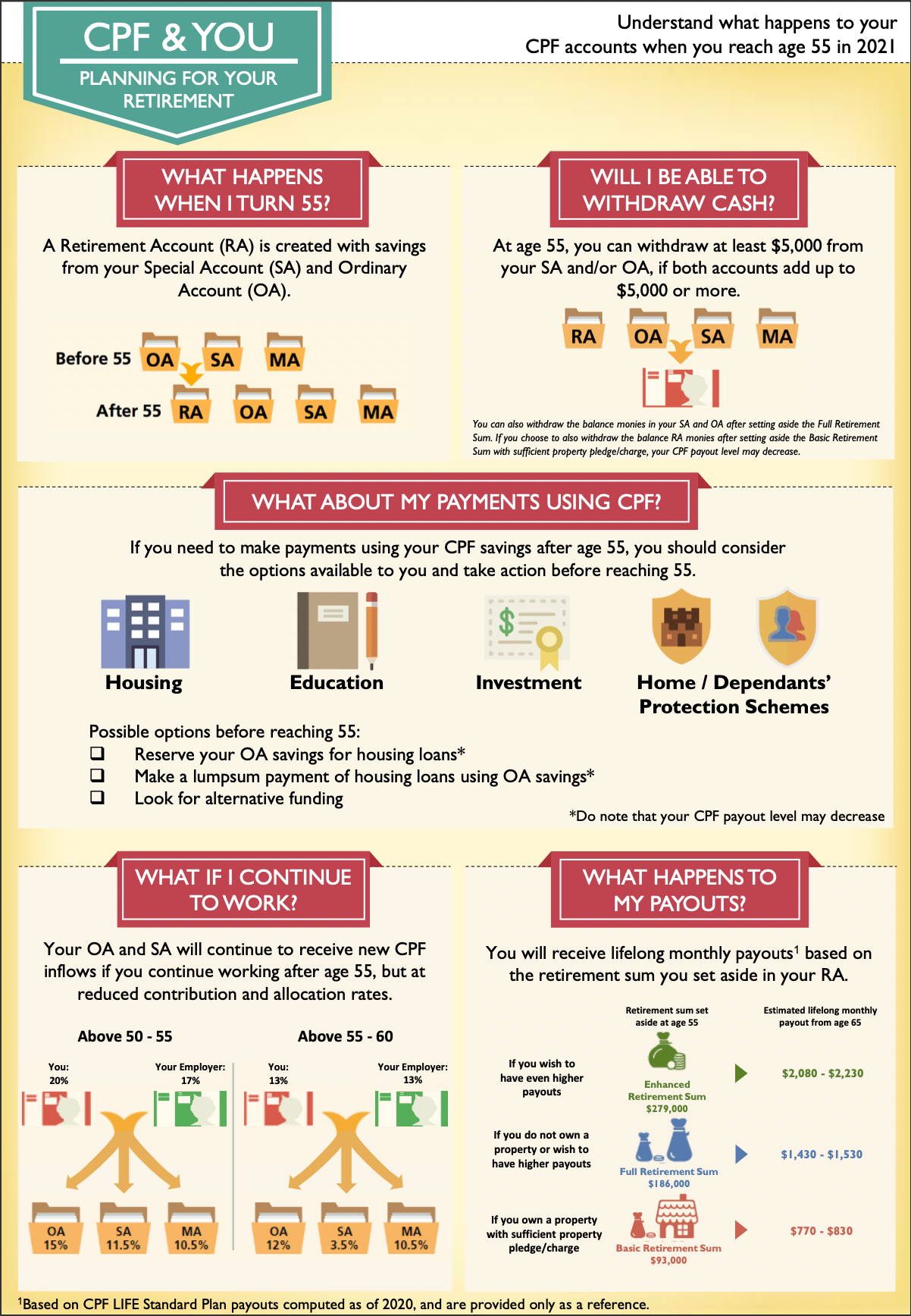

In Singapore, when you turn 55 years of age a Retirement Account (RA) will be set up for you. The funds in your RA will be made up of monies saved in your Ordinary Account (OA) as well as your Special Account (SA).

This sum is intended to provide you with a monthly income starting at your payout eligibility age (65 for people born in 1954 or later). Once your retirement monies are put aside, you would be able to withdraw the remaining funds in your OA and SA.

The three most commonly asked questions that people turning 55 ask about CPF withdrawals are as follows:

1. How much money am I allowed to withdraw?

2. Is it best for me to make a withdrawal when I turn 55?

Source: CPF

1. How much money am I allowed to withdraw?

The amount you’re allowed to withdraw starting at age 55 will depend on how much you’ve got put aside in your RA.

If you’ve already put aside an amount equal to the Full Retirement Sum (FRS): You are free to withdraw the remaining savings in your OA and SA.

If you want to exceed that amount by withdrawing more: You would be allowed to put aside an amount equal to the Basic Retirement Sum (BRS), just half the FRS, by adding a sufficient amount in terms of a property charge/pledge.

You could then withdraw the remaining funds in your RA, except for the earned interest, government grants, and top-up monies.

If your funds are under the FRS or the BRS (including property): You would be allowed to unconditionally withdraw up to $5,000.

Retirement sums for people who turned 55 in the year 2025, 2026, and 2027 are as follows:

| Year 2025 | Year 2026 | Year 2027 | |

|

Basic Retirement Sum (BRS) |

$106,500 |

$110,200 |

$114,100 |

|

Full Retirement Sum (FRS) |

$213,000 |

$220,400 |

$228,200 |

|

Enhanced Retirement Sum (ERS) |

$426,000 |

$440,800 |

$456,400 |

If you want to know the retirement sum that will apply to you, click here.

The following is an example of the above:

|

Mr. Ong reached the age of 55 in 2025 and by then his property was fully paid for. His OA had savings of $100,000 and his SA had savings of $120,000. To reach the FRS he could transfer $120,000 from his SA along with $93,000 from his OA into his RA, for a total sum of $213,000.

Option #1: Keeping $186,000 in his RA to maintain the FRS while withdrawing $7,000 out of his OA. |

2. Is it best for me to make a withdrawal when I turn 55?

It all depends on where you personally stand financially. If you do not need the money at that time, you can certainly choose to wait. Just leave the funds in your CPF accounts until later.

You are allowed to withdraw the funds any time after the age of 55. You can withdraw part or all of the funds as often as you please as long as you follow the withdrawal conditions that apply.

If you decide to hold off on making a withdrawal until later, your CPF account will keep earning interest at the rate of 6% per year.

In determining whether to make a withdrawal or not at age 55, you would want to consider what you have planned for your retirement. Remember that when you withdraw more at age 55, you will be putting aside less money for your retirement. The result would be a lower monthly payout.

3. How are withdrawals made?

The CPF Board will send you a letter about six months before you turn 55 explaining your options. When you are ready to withdraw money, go to my cpf Online Services and fill out an application. The money will then be transferred to you through GIRO or PayNow.

For further information on withdrawing funds from your CPF savings, click here.

If you still have questions or concerns, we invite you to view the video below to see a visual demonstration of the withdrawal options available to you.

Disclaimer: The information provided in this article does not constitute legal advice. We recommend that you get the specific legal advice you need from an experienced attorney prior to taking any legal action. While we try our best to make sure that the information provided on our website is accurate, you take a risk by relying on it.

At Pinnacle Estate Agency, we strongly believe in sharing our real estate knowledge to the public. For more content like this article, check out our Singapore Property Guides.