4 Examples of How CPF Accrued Interest Can Impact You

This article explains what CPF Accrued Interest is, method of computation, and uses 4 examples to show how it can impact property owners

If you have taken money out of your CPF Ordinary Account (OA) to use for the down payment and/or monthly mortgage payments in order to purchase your house, you must return every dollar you’ve withdrawn plus the 2.5% accrued interest. However, if you plan on never selling your home, there is no requirement to repay the accrued interest, so there is no need to worry about that.

This article discusses four examples of accrued CPF interest and explains how these possible scenarios could affect your finances if you end up selling your house.

Accrued Interest in CPF

The accrued interest in CPF is the amount of money your CPF savings would have earned in interest had you not withdrawn some to pay for housing. These housing payments include the money used from your CPF OA for the down payment and any money that you used for mortgage payments on your home.

Because the purpose of CPF is to make sure that Singaporeans and Permanent Residents save for retirement, the amount withdrawn plus interest must be repaid to their CPF account when the house is sold. Once you retire the funds will be returned to you upon setting the Full Retirement Sum.

How is the CPF Accrued Interest Calculated?

Because the accrued interest in CPF is the amount of money your CPF savings would have earned in interest had you not withdrawn any, you would use a 2.5% per annum to calculate the amount. If you took out $200,000 for your down payment when you bought your home and sell it after five years at the end of the minimum occupancy period, the amount of accrued interest you would need to repay is:

Accrued interest for:

1st year: $200,000 x 2.5%/year x 1 year = $5,000

2nd year: ($200,000 + $5,000) x 2.5%/year x 1 year = $5,125

3rd year: ($205,000 + $5,125) x 2.5%/year x 1 year = $5,253.13

4th year: ($210,125 + $5,253.13) x 2.5%/year x 1 year = $5,384.45

5th year: ($215,378.13 + $5,384.45) x 2.5%/year x 1 year = $5,519.06

Total accrued interest: $26,281.64

Therefore, the total amount of money you would have to repay CPF would be the $200,000 you withdrew plus $26,282.64 in accrued interest when your home is sold. At that point, the full amount in your CPF account could be used to buy your next home.

To save you the trouble of having to make the calculations yourself, you can go to the my CPF Online Services portal, which can be found under My Statement --> Section C --> Property --˘ My Public Housing Withdrawal Details.

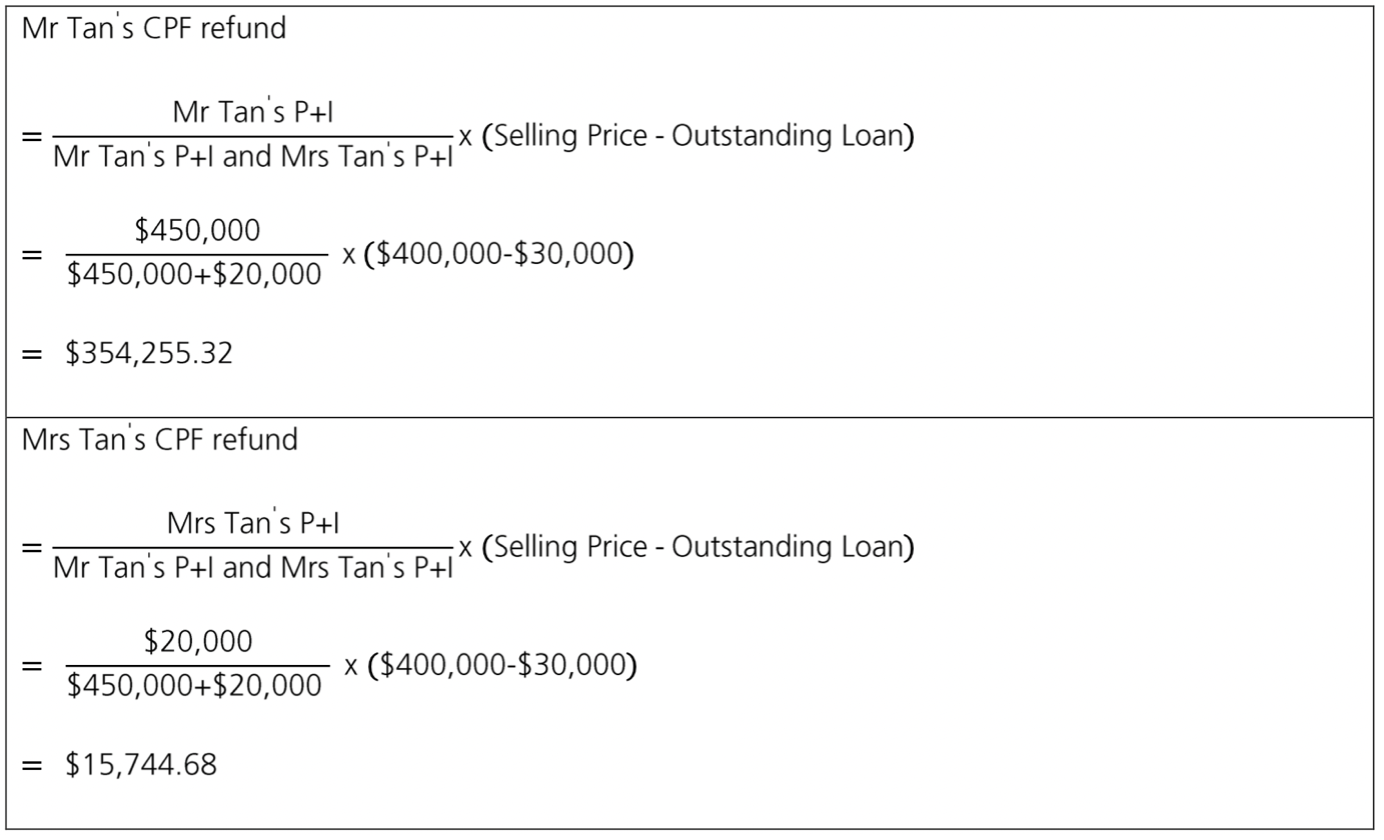

In our first example, we have Mr. and Mrs. Tan who are living in the first home they ever bought. They are both in their mid-30s and they want to determine how much CPF accrued interest they will be required to repay if they end up selling their home in the following situations:

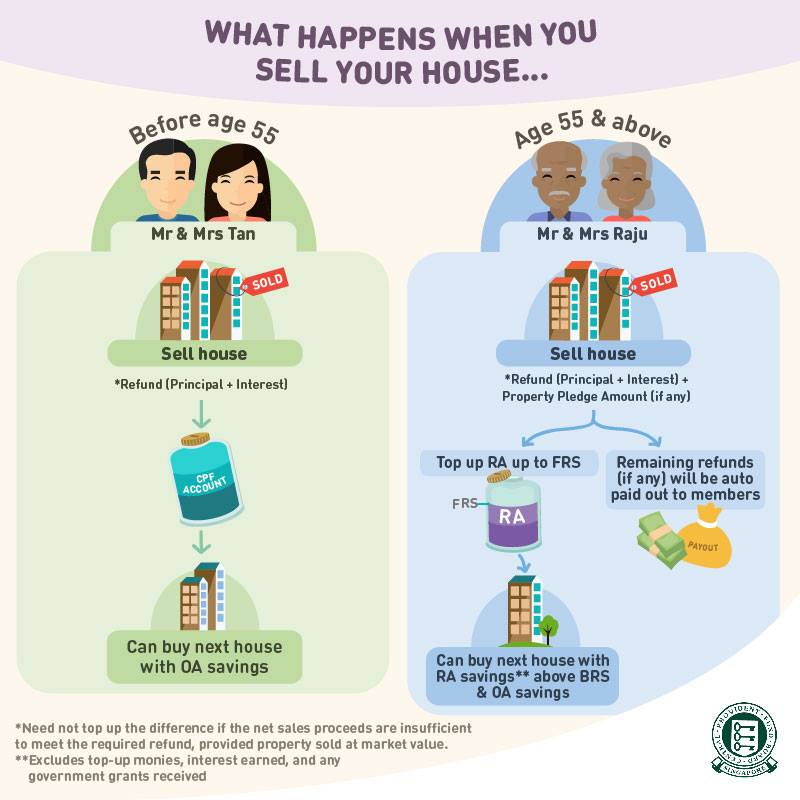

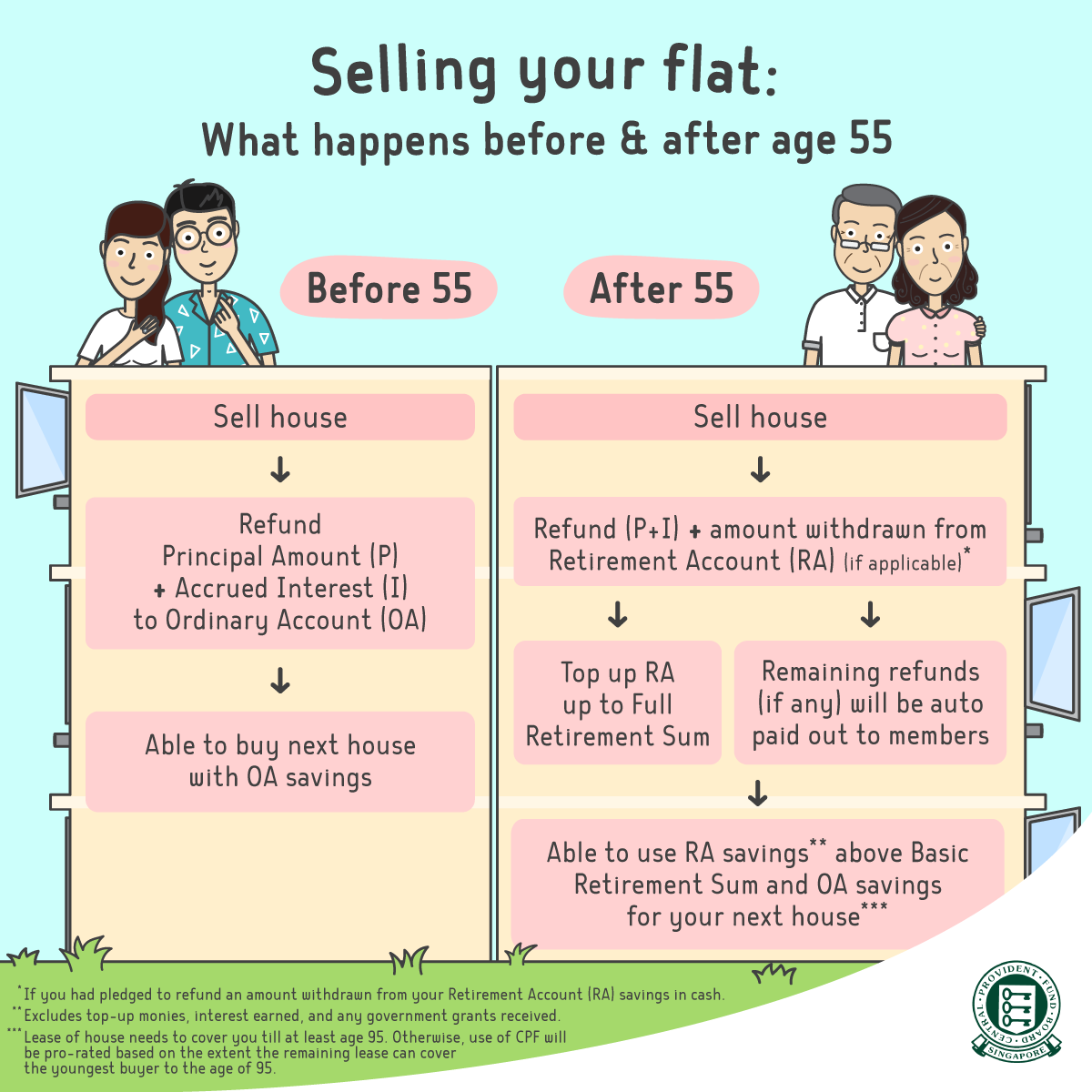

1. Selling Their Home Before Turning 55 to Buy a Larger Home

Situation:

Mr. and Mrs. Tan withdrew money from their CPF OA to finance the down payment of their first flat and for mortgage payments. They are under 55 years of age and want to sell this home, so they can buy a larger one.

|

Selling Price |

S$ 400,000 |

|

Valuation Price |

S$ 390,000 |

|

Outstanding Loan |

S$ 30,000 |

|

Mr Tan’s CPF principal amount withdrawn plus accrued interest (“P+I”) |

S$ 450.000 |

|

Mrs Tan’s P+I |

S$ 20,000 |

|

Option monies already received in cash from the buyers |

S$ 5,000 |

When the flat sells, if the price it sells for (including the option fee paid) is not sufficient (after paying what’s owed on their home loan) to fully repay the CPF, they would not need to pay the shortfall in cash if the amount their home sells for is at or above market value.

However, in these situations, any option monies paid in cash, which would include the option fee plus the option exercise fee, from the buyers when the property is sold are part of the selling price. These funds must be repaid to the sellers’ CPF accounts before the sale can close. The amount refunded will be repaid to all sellers’ CPF accounts in the correct proportions.

How 2.5% Accrued Interest Would Impact this Situation:

In Mr. and Mrs. Tan’s situation above, after they pay off their outstanding loan, proceeds from the sale would be S$400,000 – S$30,000 = S$370,000. The amount they would need to refund CPF would be S$470,000, which is S$100,000 more than they received from the sale.

Since their home is selling above market value, they as the sellers are not required to pay cash for the S$100,000 shortfall (S$470,000 – S$370,000). But Mr. and Mrs. Tan would be required to repay the option monies they received of S$5,000 to their CPF accounts because this is deemed part of the selling price.

Thereafter, the amount of CPF refunds Mr. and Mrs. Tan would be credited for in their CPF accounts would be as follows:

2. Selling Their Home After Age 55 to Purchase a Larger Home

Situation:

Mr. and Mrs. Tan chose to hang onto their home because they wouldn’t come out ahead financially if they decided to sell. In the meantime, Mr. Tan went back to university to earn a Law degree and is now a Partner at an esteemed Law Firm making twice the money he was when they first bought their home. They are both past 55 years of age when they decide it’s time to sell their home.

How 2.5% Accrued Interest Would Impact this Situation:

When people reach 55 years of age, it is expected that they would have a minimum Full Retirement Sum (FRS) in their CPF account, which is $186,000 in 2021. They are allowed to pledge half this amount against their home while keeping the Basic Retirement Sum (BRS), which is $93,000 in 2021. The BRS increases every year to keep up with inflation, cost of living, and etc. Upon the sale of their property, they must repay the amount taken out plus accrued interest as well as any amount taken out of their Retirement Account (RA).

Therefore, once Mr. and Mrs. Tan reach 55 years of age and decide to sell their property, they will be required to refund their CPFs, as follows:

- the principle amount (P) that has been taken out to buy the property;

- the 2.5% accrued interest (I); and

- the amount pledged, if they had pledged to repay a cash withdrawal from their Retirement Account (RA).

The amount refunded would be for topping off their RAs to reach their FRSs and any remaining balance would have to be paid to them in cash. They could then use what was saved in their RAs over the BRSs to purchase their next home if it is enough to last them until they are 95 years old!

3. Need to Sell Their Home to Settle a Divorce

Situation:

Mr. and Mrs. Tan are unhappy in their marriage and are getting a divorce and are selling their matrimonial home. Both had contributed equally to the purchase, but since they could not agree on how to divide their assets, the court will decide on the split.

How 2.5% Accrued Interest Would Impact this Situation:

Because of the Women’s Charter, the returns from selling the flat may not be equally divided since it depends on several factors that must be considered by the court.

Since Mr. and Mrs. Tan could not agree on how to divide the returns, the court must decide. In making this ruling, the court will consider how much money each party contributed to buy the flat, whether they have children, how long the marriage lasted, and etc.

The final determination could be that the proceeds from the home are unequally split, maybe 60-40 rather than 50-50. The CPF refunds will reflect the same split as the proceeds if the proceeds from the sale after paying off the mortgage is sufficient to make the necessary CPF refund to both parties’ CPF accounts.

What if the proceeds from the sale are insufficient to refund the CPF OAs?

No matter what the court orders regarding the split, the CPF Board requires that a proportionate refund be made of the amount withdrawn plus 2.5% accrued interest to both Mr. and Mrs. Tans’ CPF accounts.

4. Looking to Buy Their First Home

Situation:

Mr. and Mrs. Tan’s son Alex is 26 years old and is planning on buying his own home since his parents are divorcing. He is trying to figure out how to finance the purchase of his first home.

How 2.5% Accrued Interest Would Impact this Situation:

Alex must determine how much of his CPF to use for the purchase of his first home. If his plan is to never sell this house, it won’t matter where he gets the down payment unless he is irresponsible about saving money and could end up struggling after he retires. If this is the case, he should plan on repaying his CPF before retirement.

On the other hand, if Alex expects to sell his property at some point, he should consider that the funds remaining in his CPF can currently earn as much as 5% a year in a Special Account. Therefore, the cost of using his CPF funds to buy the house might not be worth the aggravation of repaying this accrued interest later on.

If the house sells below market value (at a loss), he would be forced to pay cash to offset the cost of the interest his funds would have earned had they’d stayed in his Retirement Fund instead of being used to buy the house.

If you were Alex, one solution might be to split the monthly mortgage instalments between CPF and cash in paying off the mortgage. This would lower the accrued interest owed when the property sells.

For more information, please read another article on Does it Make Sense to Spend All the Funds in Your CPF OA on Your HDB Flat?

Key Takeaways Regarding the Impact of CPF Accrued Interest

1. Pay Cash or Use CPF?

If you have plenty of cash on hand it may make sense to use cash instead of withdrawing funds from your CPF, especially if your cash would otherwise languish in the bank. Allowing your CPF funds grow by 2.5% a year is clearly better than you would get from the low interest rate of no more than 1% that banks typically pay.

However, if you are a talented investor who is confident about your ability to earn more on your investments than what CPF can offer, then limit your use of cash since the return on your investments may be more than your CPF accrued interest.

It is important that you calculate your accrued interest ahead of time, so that you know the financial ramifications of withdrawing money from your CPF OA for the down payment and/or monthly mortgage payments on your home. If you leave it there and use cash instead, your CPF funds will grow by 2.5% annually due to the accrued interest.

2. Consider Repaying Your CPF Partially or In Full

You can lessen the amount of accrued interest owed by making repayments to your CPF whenever possible. The longer you delay repaying your CPF, the more you will owe in the future. Keep in mind though that you must balance the advantages that cash in hand gives you now against the benefits of repaying your CPF. If you have a promising investment you could make with the cash you have, that might be your best option. However, you need to weigh this against how much you could afford to repay your CPF and when.

3. Ask a Professional for Help Sorting Out Your Finances

Instead of trying to figure all this out on your own, you can turn to Pinnacle Estate Agency for the financial advice you need regarding your CPF. We will look at your overall financial situation including the valuation on your home and current savings to come up with affordable mortgage options for financing your home rather than using your CPF.

There is always some flexibility in repaying CPF and in determining when the best time to sell your home would be. It only makes sense to understand the situation you would be getting yourself into before you make such important decisions. You need to weigh the potential benefits against the risks. Strategic financial planning can help make the first property you sell benefit you financially as much as possible, now and in the future.

At Pinnacle Estate Agency, we strongly believe in sharing our real estate knowledge to the public. For more content like this article, check out our Singapore Property Guides.