CPF Refunds: What Happens When You Sell Your Flat Before and After Age 55

This article discusses the difference in CPF refunds requirement when you sell your flat before and after the age of 55

Are you thinking about selling your flat? If so, have you figured out how much CPF you’ll be allowed to use to buy your next home?

This shows what will happen to your finances if you sell your flat before reaching 55 as opposed to waiting until afterwards:

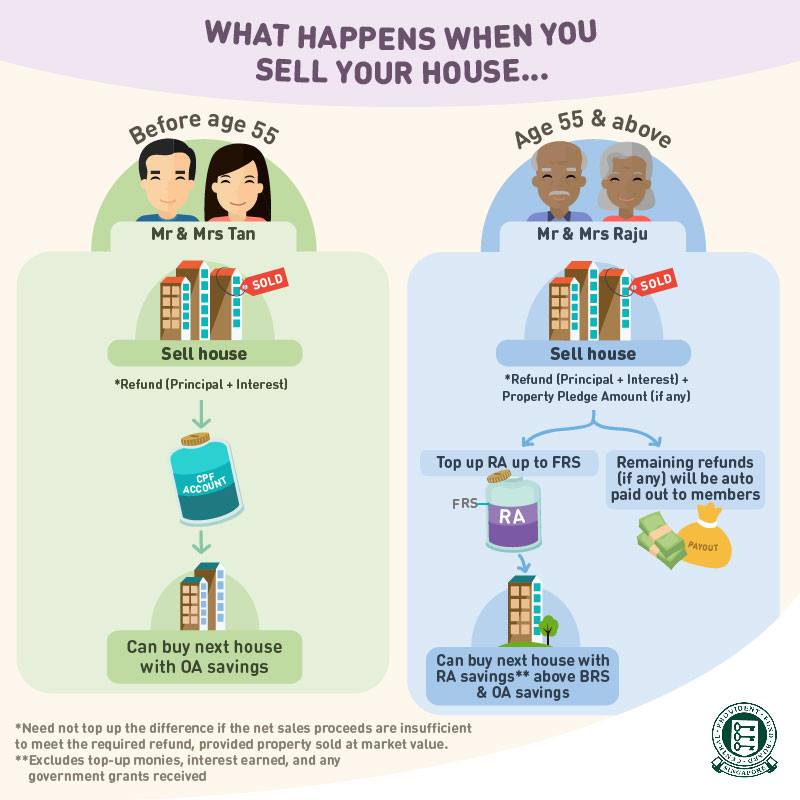

Selling Before Reaching 55 Years of Age

If you decide to sell your flat prior to reaching 55, you are required to repay your Ordinary Account (OA):

- principal (P) amount you took out of your OA to pay for the flat; and

- accrued interest (I) on the funds you took out, which is how much it would have earned had you left the money in your OA.

Repaying these funds ensures that there will be sufficient savings in your OA for your future, whether you need it to buy another home or to support you when you retire.

So, don’t forget that you retain the option of using your OA savings to help pay for your next house.

Selling At Age 55 or Older

If you wait to sell your flat after reaching 55, you are required to repay your CPF:

- principal (P) amount you took out to pay for your flat;

- accrued interest (I); and

- amount you pledged, if you made a pledge to repay the amount you took out of your Retirement Account (RA) in cash.

The amount you refund will top up your RA, so that it has the Full Retirement Sum (FRS). If there is a balance, you will receive it in cash. You are then allowed to use your RA funds over the Basic Retirement Sum (BRS) to help pay for your next house if it will last you until you reach 95 years of age.

Retirement sums for people who turned 55 in the year 2025, 2026, and 2027 are as follows:

| Year 2025 | Year 2026 | Year 2027 | |

|

Basic Retirement Sum (BRS) |

$106,500 |

$110,200 |

$114,100 |

|

Full Retirement Sum (FRS) |

$213,000 |

$220,400 |

$228,200 |

|

Enhanced Retirement Sum (ERS) |

$426,000 |

$440,800 |

$456,400 |

If you want to know the retirement sum that will apply to you, click here.

By replenishing your RA in this manner, you will be more financially secure as you get up in years.

You are now allowed to use funds in your CPF up to whichever amount is lower, the purchase price or the assessed value of the flat at the time the purchase is being made. This holds as long as the time remaining on the lease would extend until the youngest buyer reaches the age of 95. If not, the amount of funds you can use from your CPF will be pro-rated. So, remember to check how much time still remains on the lease when choosing your next flat.

If you are curious about what your principal and interest come to, there is no need to do the calculations. Just login to my CPF Online Services and it will show you how much you have withdrawn so far for housing.

Disclaimer: The information provided in this article does not constitute legal advice. We recommend that you get the specific legal advice you need from an experienced attorney prior to taking any legal action. While we try our best to make sure that the information provided on our website is accurate, you take a risk by relying on it.

At Pinnacle Estate Agency, we strongly believe in sharing our real estate knowledge to the public. For more content like this article, check out our Singapore Property Guides.