Cost of Purchasing and Owning a Property in Singapore

This article discusses all the cost of purchasing and owning a real estate that all property buyers have to take note of.

Are you looking to purchase your first property in Singapore? Here we list down on all the cost of purchasing any type of property in Singapore including HDB flats, and private residential, commercial, or industrial property. The journey does not end here, as owning a property also incurs cost over time. Fret not, we got all covered for you!

Cost of Purchasing a Property:

1. Stamp Duty

a) Buyer’s Stamp Duty (BSD)

Property buyers are required to pay BSD when purchasing a property in Singapore. BSD will be computed on the transacted price or valuation price (whichever is the higher amount). There is a slight difference in the BSD rate for residential and non-residential i.e. commercial or industrial properties.

As of 14 February 2023, revised BSD rates came into effect, which are as follows:

| Purchase Price or Market Value of the Property | BSD Rates for residential properties | BSD Rates for non-residential properties |

| First $180,000 | 1% | 1% |

| Next $180,000 | 2% | 2% |

| Next $640,000 | 3% | 3% |

| Next $500,000 | 4% | 4% |

| Next $1,500,000 | 5% | 5% |

| Remaining amount (in excess of $3,000,000) | 6% | 5% |

The formula to calculate BSD Rates for residential properties:

a. BSD for S$1,000,000 and below: 3% x Transacted Price or Market Value (whichever is higher) – S$5,400. For example: (3% x 1,000,000) – S$ 5,400 = S$24,600.

b. BSD for properties between $1,000,001 to S$1,500,000: 4% x Transacted Price or Market Value (whichever is higher) - $15,400. For example (4% x 1,300,000) – S$15,400 = S$36,600.

c .BSD for properties between $1,500,001 to S$3,000,000: 5% x Transacted Price or Market Value (whichever is higher) - $30,400. For example (5% x 1,800,000) – S$20,400 = S59,600.

d. BSD for properties above $3,000,000: 6% x Transacted Price or Market Value (whichever is higher) - $60,400. For example (6% x 3,500,000) – S$60,400 = S$149,600.

The formula to calculate BSD Rates for non-residential properties is 3% x Transacted Price or Market Value (whichever is higher) – S$5,400. For example: (3% x 2,000,000) – S$ 5,400 = S$44,600.

b) Additional Buyer’s Stamp Duty (ABSD) (only for residential properties)

ABSD is a tax that’s levied on top of BSD for purchase of another residential property by property owners who already own a residential property. This is a “cooling measures” that was first introduced by the Singapore government on 8 December 2011 to ensure the residential property market didn’t create a bubble. Since then there has been many revisions to the rate according to the residency status and number of properties presently held by owners.

The current ABSD rates (with effect from 27 April 2023) from are stated in the following table:

| Profile of Buyer | ABSD Rates |

| Singapore Citizens (SC) buying first residential property | 0% |

| SC buying second residential property | 20% |

| SC buying third and subsequent residential property | 30% |

| Singapore Permanent Residents (SPR) buying first residential property | 5% |

| SPR buying second residential property | 30% |

| SPR buying third and subsequent residential property | 35% |

| Foreigners (FR) buying any residential property | 60% |

| Entities buying any residential property (plus additional 5% for housing developers, non-remittable) | 65% |

| Trustee buying any residential property | 65% |

The purpose of ABSD is to discourage people from hoarding on properties for future gains in the hope selling it at higher price. Thus, remissions are given to married couple whose intention is to purchase residential property for their own stay. Such married couple must include a Singapore Citizen (SC) Spouse. There is also remission given to married couple purchasing a second residential property with the intention to sell their first residential property.

There is no ABSD for non-residential property i.e. commercial or industrial properties.

2. Conveyancing Lawyer fee

Conveyancing lawyer service is required to transact properties to ensure the title of property is transferred to property buyers free of encumbrances. Conveyancing fee is one-off and ranges from $1,600 – $3,000 depending on the amount of the transaction, and whether there is CPF funds utilised, and mortgage financing for the purchase of the property in which they have extra work to liaise with the relevant authority and banks.

3. Mortgage Duty (Stamp Duty for Mortgage Documents)

You probably have not heard about this as your conveyancing lawyer will usually incorporate this amount in their total fee. Mortgage duty is payable on mortgage document where the interest in immovable property or shares is transferred from the borrower to the lender as security for the repayment of a loan obtained under such an agreement. Mortgage duty of 0.2% to 0.4% is payable on the loan amount, subject to a maximum duty of S$500.

4. Renovation

Unless you are purchasing a brand-new home from a show gallery from real estate developer, you may end up needing to renovate. You might purchase supposedly well-renovated house only to find out there are many unseen defects and it doesn’t look that nice without all the previous owners’ moveable furniture. If you do not plan this properly from the beginning, you may need to take up a renovation loan on top of your mortgage loan.

Cost of Owning a Property:

1. Mortgage Instalment

You will begin paying mortgage instalment on monthly basis as soon as you collect keys to your property.

2. Maintenance Fee & Sinking Fund / HDB’s Service & Conservancy Charges (S&CC)

Beside monthly mortgage instalment and utility bills, strata-titled property owners have to pay maintenance fees that form the management committee’s fund. It is intended to pay for the day-to-day short-term expenses to upkeep the common facilities and common area such as security guards, swimming pool maintenance, cleaners, gardeners, pest control, etc. Price varies based on strata development setup, shares value allocation, and it ranges from $100 up to even $1,500 per month. Usually after property reaches a certain age i.e. 10 years, property owners start paying for sinking fund to save money for future long-term expenses such as painting of buildings, replace the lift, or rejuvenate the gymnasium. Strata-titled property owners are usually billed on quarterly (3-monthly) basis.

HDB flat owners have to pay monthly Service & Conservancy Charges (S&CC) to their respective Town Councils managing the estate. The amount is much less than that of private strata-titled properties, and more often the government will give rebate on this e.g. 2-3 months rebate in a year. Price varies based on types of flats, and Town Councils, ranging from between ~ $25 – $90 per month.

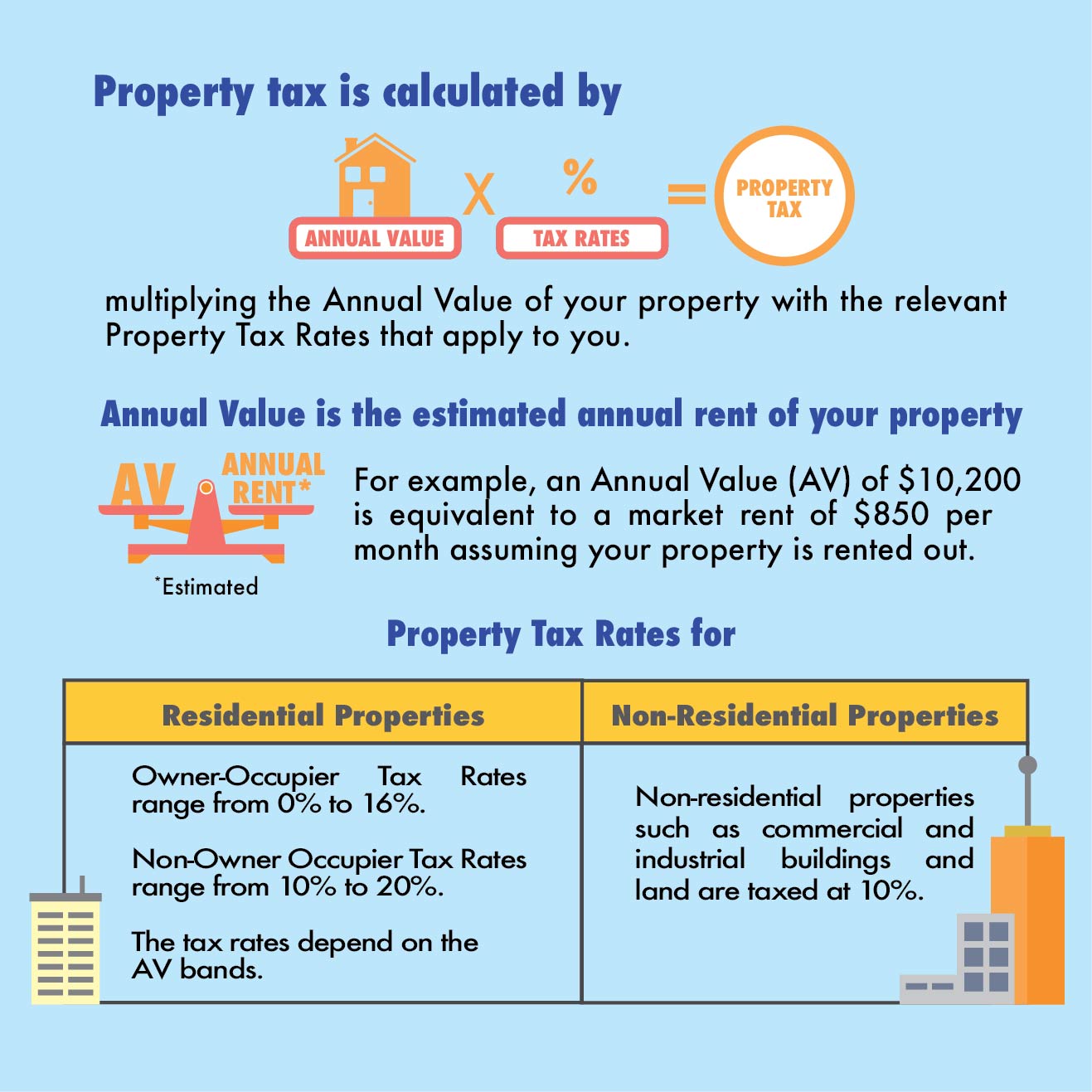

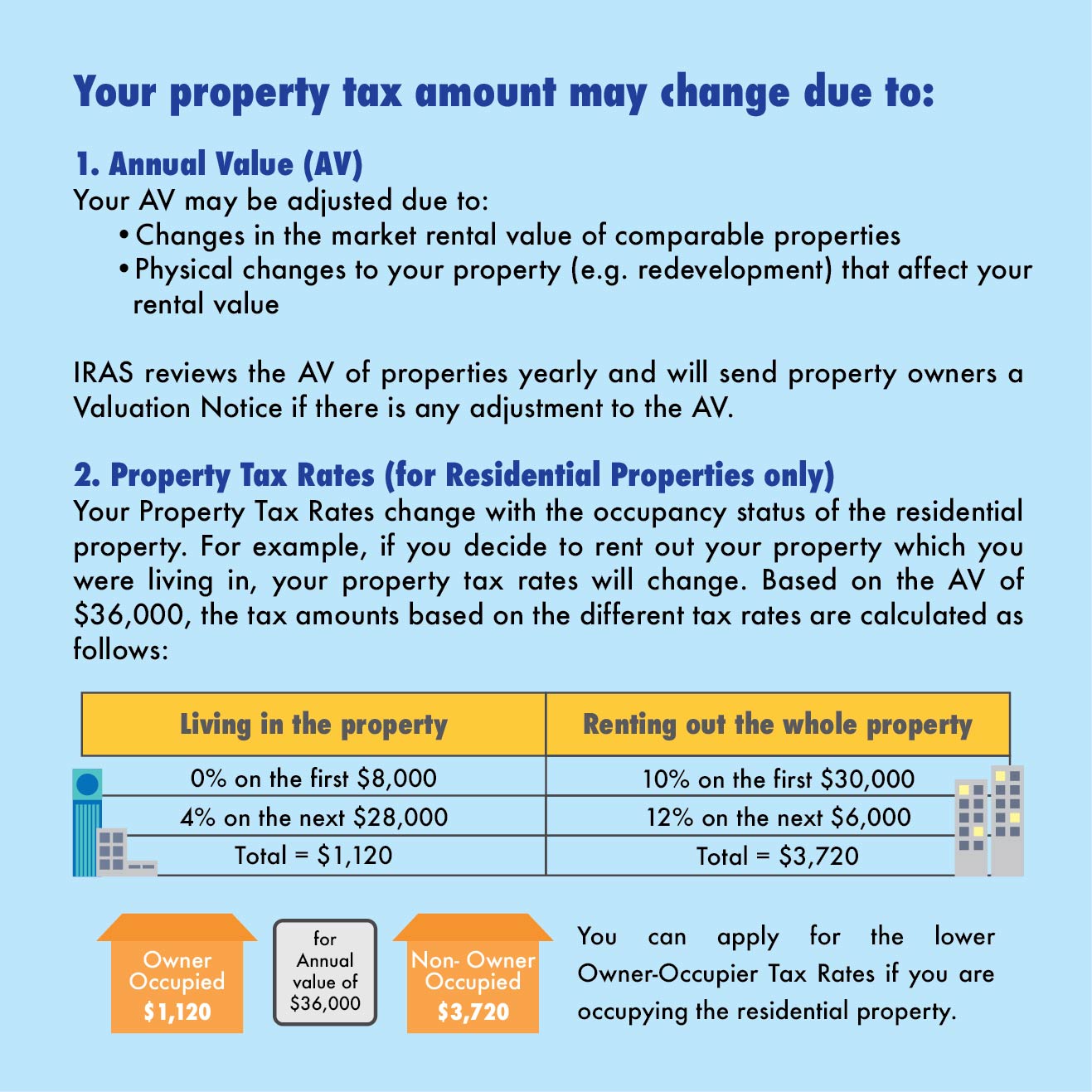

3. Property Tax

Owning a property in Singapore comes with the responsibility of paying property tax, which goes towards nation building. It applies whether the property is occupied by the owner (owner-occupied), rented out or left vacant. To encourage home ownership, the tax rate is lower for owner-occupied residential properties. HDB flat "owners" also have to pay Property Tax.

Source: Inland Revenue Authority of Singapore (IRAS)

Click here to learn the latest Property Tax Rates

Property tax is calculated by multiplying the Annual Value of your property with the relevant Property Tax Rates that apply to you. Annual Value is the estimated gross annual rent of the property if it were to be rented out, excluding furniture, furnishings and maintenance fees. It is determined based on estimated market rentals of similar or comparable properties and not on the actual rental income received. Annual Value is assessed annually and may be revised upwards or downwards or kept at the same level depending on the market values at that time. Property Tax is different from Income Tax that will be explained below.

Source: Inland Revenue Authority of Singapore (IRAS)

4. Fire Insurance

If you are financing your housing with banks or financial institutions, they made it compulsory that you have a fire insurance insuring your property against incidence of fire. The cost of fire insurance annually starts from $20. Premium is based on size of property, and coverage.

5. Mortgage Insurance

Mortgage insurance protects borrowers (who is also the homeowner) and his/her families against losing their homes in the event of his/her death or total permanent disability. You may have heard of Home Protection Scheme (HPS). It is of similar concept, except it is made compulsory by CPF to flat buyers servicing their monthly housing loan instalments on their HDB flat. HPS does not cover private residential properties or Executive Condominium. In the case of private bank loans, it is also not made compulsory by banks unlike the Fire Insurance, however it is advisable that borrowers purchase mortgage insurance. In the event of death or total permanent disability, the insurer will fully pay off the outstanding loan balance.

6. Income Tax (only for rental properties)

Income Tax is a tax on your earnings, and this include the rental income earned from renting out your property. Rental income refers to the full amount of rent and related payments property owners receive then they rent out their property. This includes rent of the premises, maintenance of the premises, furniture and fittings. There are deductible expenses such as your housing loan interest, property tax, fire insurance, repairs, maintenance, replacement of furniture and fittings. To simply claim for the deductible expenses, IRAS allow residential property owners to claim 15% deemed rental expenses. Commercial and industrial property owners do not have this simplified claim option. Click here for more info on IRAS website.

At Pinnacle Estate Agency, we strongly believe in sharing our real estate knowledge to the public. For more content like this article, check out our Singapore Property Guides.