Complete Guide to Buying HDB Resale Flat

Find answers for all your first time HDB Resale buyer questions about eligibility, resale procedures, mortgages, downpayment, and many more.

Do you want to own an HDB flat but have no patience to keep waiting for years until you can move in to new Build-To-Order (BTO) flat? Here’s a good news, that’s not the only option available – you can always go for an HDB resale flat.

This article will cover the basics of what HDB Resale flat is, the advantages and disadvantages of purchasing one, different schemes you can take advantage of to finance your purchase, eligibility criteria, and other important HDB resale procedures.

Here we go then!

Eligibility to Buy Resale HDB Flats

Minimum Occupation Period for an HDB Resale Flat

What is an HDB resale flat?

An HDB resale flat is a flat that is currently owned by another individual who bought it either directly first hand from HDB or second hand from another owner. To qualify as a resale flat, the individual must have completed the 5 years Minimum Occupation Period (MOP) residing in the flat.

Buying a resale flat transfers the remaining lease to your name. Once the purchase transaction has been successfully completed, you must occupy the flat and not allowed to let out the whole flat or sell within the 5 years MOP.

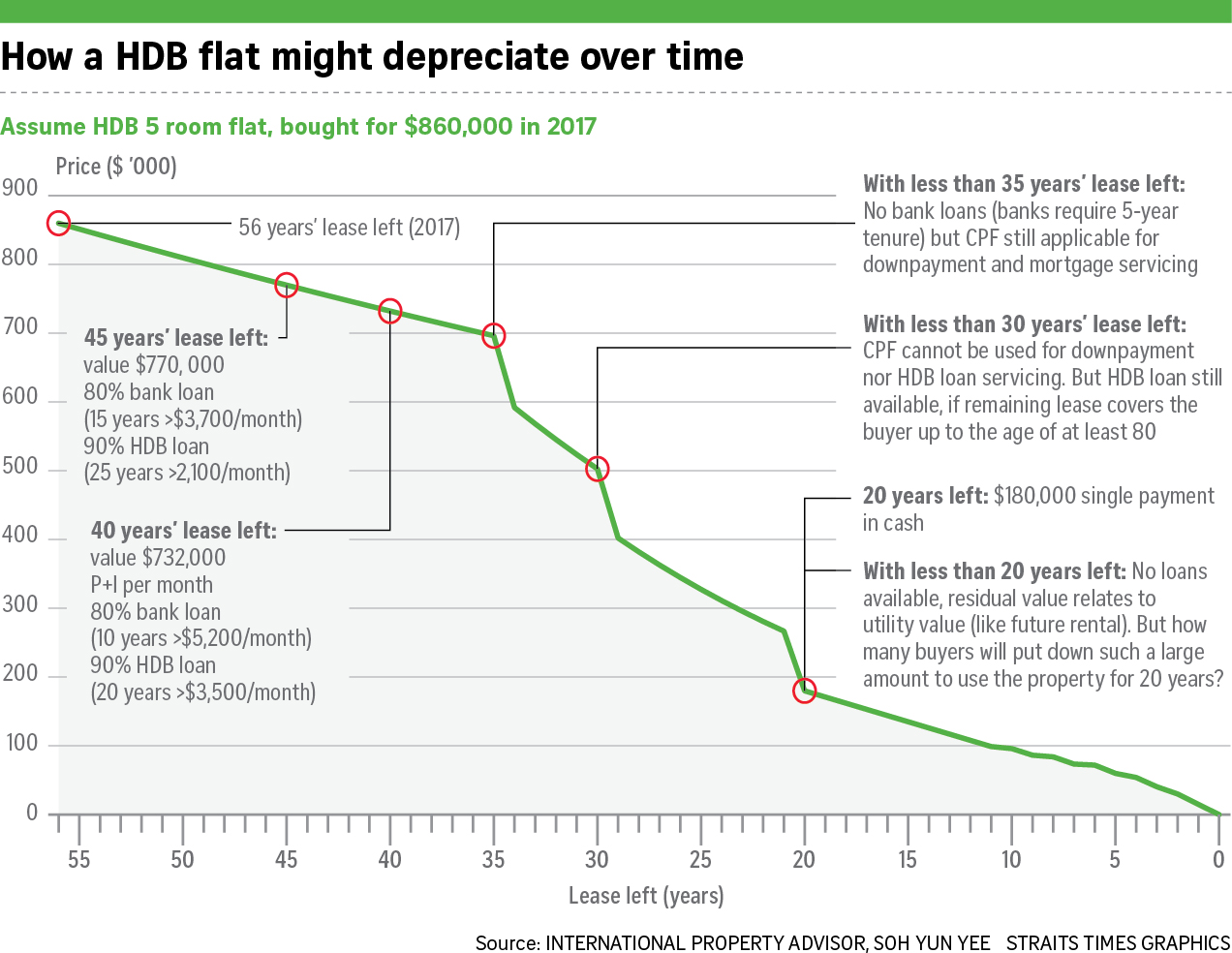

Unlike a brand-new BTO flat, a resale flat doesn’t come with fresh 99-year lease. As a flat gets older, the lease period gets correspondingly shorter. Therefore, it’s important to take the remaining lease period into consideration before you purchase an HDB resale flat.

Do note that renovating an HDB resale flat can be more expensive than renovating a comparative BTO flat as you’ll also need to modify or remove renovations made by the current owner.

We’ll be covering the advantages and disadvantages of HDB BTO and resale flats in greater detail down this article.

Eligibility to Buy Resale HDB Flats

To be eligible for an HDB resale flat in the open market, prospective buyers need to fulfil the following criteria:

- The resale flat application must have at least 1 Singapore Citizen or 2 Singapore Permanent Residents

- The applicants must be at least 21 years of age if the application is made as part of a family nucleus. The minimum age limit is 35 years if the applicant is single. For single applicant, he/she must be a Singapore Citizen.

- The applicants should not own other residential units/houses/land in Singapore or overseas. If you do, you shall undertake to sell it within six months of the purchase of your resale flat.

Income ceiling

Unlike BTO flats, there is no income ceiling as criteria for purchasing HDB resale flats. However, keep in mind that income ceiling limits apply for HDB Concessionary Home Loan and CPF Housing Grant.

Additionally, applicants need fall under any one of the following eight schemes before they’re eligible to purchase an HDB resale flat:

|

Which of these apply to you? |

HDB scheme |

|

If you’re looking to buy a flat with a family member, spouse, parent, or children |

Public Scheme |

|

If you’re engaged and looking to buy a flat with your fiancé |

Fiancé/Fiancée Scheme |

|

If you’re above 35 years old and not married or engaged |

Single Singapore Citizen Scheme |

|

If you’re single want to buy a flat with other single friends |

Joint Singles Scheme |

|

If you’re married buy your spouse is not a Singapore Citizen or Permanent Resident |

Non-Citizen Spouse Scheme |

|

If you're Single Singaporean applicants whose family members aren’t Singaporean citizens or Permanent Residents |

Non-Citizen Family Scheme |

|

If you’re orphaned siblings who are also single but looking to purchase an HDB resale flat jointly |

Orphans Scheme |

|

If you’re wish to purchase adjoining 3-bedroom or smaller flats with the intention of combining them into a single unit are covered by this scheme. |

Conversion Scheme |

The official HDB portal offers more details about the eligibility criteria for various schemes.

Check Ethnic and PR quota too!

Applicants need to ensure that the ethnic quota for the flat they’re eyeing is open for their races. If the application lists a non-Malaysian permanent resident, it’s crucial to ensure that the local PR quote hasn’t been exceeded as well.

The PR and ethnic quotes are periodically updated every month, which affects all HDB resale applications made during that particular month. Therefore, you might need to keep yourself updated regarding the quota for the neighbourhood/block you’re looking to buy an HDB resale flat in, so as to not face troubles later on.

Enquiry on Buyer's Eligibility under the Ethnic Integration Policy and SPR Quota.

Minimum Occupation Period (MOP) for an HDB Resale Flat

Aside from the general eligibility criteria, flat buyers also need to be aware of the five (5) years Minimum Occupation Period, aka MOP, from the date of purchase.

The buyers are legally required to reside in the flat throughout the entire MOP period unless there’s an exception that disables them from doing so. In such cases, HDB approval must be sought and the unit cannot be rented out to anyone else. Room rentals are permitted under condition that the buyer(s) also reside(s) in the flat.

Can PRs purchase HDB flats?

Permanent Residents or PRs who wish to purchase an HDB flat are only allowed to purchase HDB resale flats. They are also required to fulfil the following conditions:

- A minimum age of 21 years.

- Obtained the permanent residency status for at least three years.

- Purchase with a fiance or family member under Fiancé/Fiancée Scheme and the Public Scheme

- They cannot own any residential properties, both in Singapore and overseas. Should they own any properties, these need to be sold off within six of the date of purchase. However, PRs are free to acquire other properties once the MOP period is over.

Upon completing the Minimum Occupation Period of 5 years, PRs are not allowed to rent their flat out. Having said that, PRs are allowed to purchase another residential property i.e. for investment or sell the flat.

HDB Resale Procedure

How Long Is The HDB Resale Flat Purchase Process?

The latest user-friendly and streamlined HDB Flat Portal has simplified the purchasing process to a great extent. Generally speaking, the entire process shouldn’t take you more than 12 weeks excluding the very first things you need to do which is to apply for HDB Flat Eligibility (HFE). Afterwards, it all comes down to how quickly the buyer can select a flat and complete their negotiations to seal the deal.

Now, we’ll move on to a comprehensive discussion of the different steps associated with the HDB resale process. Here are all the 10 steps of the HDB resale process, in order:

1. Apply for HDB Flat Eligibility (HFE)

2. Estimate Your Financial Condition And How To Finance Your Loan

3. Gather More Information About Properties in Your Preferred Areas

4. Choose Whether to Engage A Real Estate Agent or Do Everything On Your Own

6. Get an Option to Purchase (OTP)

7. Submit A Request for Valuation

9. Submit Your Flat Resale Application

10. Endorse the Resale Documents and Pay Applicable HDB Legal Fees

11. Carry out A Flat Inspection

12. Attend the Flat Resale Completion Appointment

1. Apply for HDB Flat Eligibility (HFE)

You will have to get an HDB Flat Eligibility (HFE) letter ahead of time, whether you’re looking for a resale or BTO flat. Your HFE letter will provide you with an overall understanding of the process as well as the housing and financing options available to you. Please note that it takes about 21 working days (or about a month calendar days) to obtain an HFE letter, and it may take longer in the month when there is launch of BTO and SBF flats. Without HFE letter, you are unable to proceed with any purchase meaning unable to pay $1,000 Option fee to obtain an Option to Purchase from any resale seller.

The HDB Loan Eligibility (HLE) has now been replaced by the HFE letter. Previously, the eligibility of prospective homebuyers to buy an HDB flat, get grants, and take out a housing loan was evaluated at various stages of the buying process. But now the process has been streamlined, so that there is only one application, making it all the more convenient. This letter informs prospective flat buyers ahead of time what their eligibility is for buying a resale or new flat, getting an HDB home loan, and CPF housing grants, including the loan and grant amounts.

Prior to the implementation of the new HFE process on 9th May 2023, people applying to buy a resale or new flat, would not have their eligibility to buy the flat or housing grants confirmed. This led to a great deal of uncertainty and anxiety among buyers.

HDB has streamlined the flat buying process with this newly introduced HFE letter. The various eligibility assessments for purchasing an HDB flat, HDB housing loans, and housing grants have been consolidated into just one online application via the HDB Flat Portal. The result will be more convenience and certainty for flat buyers, giving them more clarity ahead of time on what their housing budget is as well as their financing options. With this information flat buyers can make more sensible decisions regarding their purchase.

If you are thinking about taking out a loan from a bank or other financial institution (FI), you can also apply to participating FIs for an In-Principle Approval at the same time you are applying for an HFE letter. Your letter will also indicate a loan assessment.

How to Apply for an HFE Letter?

Follow these two steps in applying for an HFE letter:

|

Step 1. Complete a preliminary HFE check.

|

Read our article on detailed guidance on how to apply for an HFE letter

2. Estimate Your Financial Condition And How To Finance Your Loan

Once you have obtained an HFE letter, you will have clear picture of loan amount you are able to take, and CPF grants amount that you are eligible for. If you are not taking HDB loan, you have to separately apply to banks to obtain Approval-in-Principle to learn the maximum loan amount the bank can grant you. You can read more on the difference between a bank loan or an HDB loan.

Take note that the Loan-to-Value ratio for HDB and bank loan are not the same at 75%. Thus if you are eligible for the maximum 75%, the downpayment will be 25% which can entirely be paid by CPF. For bank loan however, there is requirement for minimum of 5% to be paid in cash, whereas the 20% can be in combination of cash and CPF. HDB is known to be more lenient in terms of repayment matters.

In addition to loan amount and CPF grants, to learn how much you can afford and thus determine what types of flat you are targeting, do a comprehensive financial health check first. Here are the most important considerations:

- How much do you have in CPF/savings?

- How much debt do you currently have (car loans, credit card debt, etc.)?

- How much do you save every month?

- How much disposable income can you spare towards your home loan payments?

- How much are you eligible for in HDB grants?

The property’s purchase price isn’t the only payment you’re going to have to make. Other expenses like renovation costs, home insurance, stamp duty, HDB legal fees, etc. need to be accounted for as well. You’re allowed to utilize the savings present in your CPF Ordinary Account (OA) for paying the down payment and monthly mortgage payments of your resale flat. Applicants who are using an HDB Housing loan to finance their purchase has the option to fully drain or retain a maximum of $20,000 in their CPA OA Account. If the flat has a remaining lease period of fewer than 60 years, there is withdrawal limits imposed on the CPA OA account.

Payment breakdown

Here’s a comprehensive breakdown of the different types payments you'll need to make:

|

Payments to be made |

Payment mode |

How much to pay? |

When to pay? |

|

Deposit to Seller: |

Cash |

Up to $5,000 in total, paid in 2 stages. Amount can be negotiated with the seller, and is taken off the resale price. 2) Option exercised fee payable of up to $4,999 Both 1) & 2) combined forms the Deposit which shall not be more than $5,000. |

Option fee in exchange of Option to Purchase, and Option exercise fee within 21 days later |

|

Downpayment |

CPF/Cash |

HDB loan 25% (including $5,000) of transaction or valuation price whichever is lower can be paid via CPF&/orcash Bank loan 25% (including $5,000) of transaction or valuation price whichever is lower, 5% (including the $5,000) must be paid in cash, whereas the remaining 20% can be paid in CPF &/or cash. |

HDB loan: Once you confirm your financial plan through the HDB Flat Portal Bank loan: Depending on Bank |

|

Valuation fee |

Credit Card |

$120 |

Within the next day upon receiving HDB Option to Purchase from the flat seller |

|

Resale application administrative fee |

Credit Card |

$40 (1-2 room) |

When submitting HDB Resale Application |

|

Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) |

Cashier’s order |

Buyer’s Stamp Duty (BSD) Payable: Next $500,000: 4% Next $1,500,000: 5% Thereafter: 6% Additional Buyer’s Stamp Duty (ABSD) Payable: SC-SC buyers: no ABSD SC- SPR buyers (considered Singapore Citizens household): no ABSD SPR-SPR buyers (both applicants must have received 3 years receiving SPR status): 5% ABSD |

Within 14 days upon HDB in-principle approval |

|

Stamp Duty on Mortgage |

Cashier’s order |

0.2% of the loan amount capped at $500 |

Within 14 days upon HDB in-principle approval

|

|

Legal fees |

Credit Card for HDB Loan, Cashier's Order / CPF for Bank Loan |

When taking HDB home loan: 2. Registration fee: ~$38.30 3. HDB Caveat Registration fee: ~$64.45 when signing Agreement of Lease 4. Survey Fee: 1-Room: $150 2-Room: $150 3-Room: $212.50 4-Room: $275 5-Room: $325 Executive Flat: $375 5. Stamp Duty Fees 0.4% of loan amount (cap. $500) *You can find out more at the HDB Legal Fees Enquiry Page

When taking Bank loan Legal fees (facilitated by an external conveyancing law firm ): ~$2,500 for their services |

A step right after acknowledging documents on HDB Flat Portal (prior to HDB approval) |

|

Fire Insurance |

Cash / Credit Card |

Starts from ~ $1.62-$8.10 for a 5-year premium with FWD Insurance |

On resale completion appointment |

|

Home Protection Screen (HPS) |

Cashier’s order |

Can be calculated individually using the CPF HPS Premium Calculator |

On resale completion appointment |

|

Cash payment for balance purchase price (if applicable) |

Cashier’s order |

The difference between the resale price and the market valuation |

On resale completion appointment |

Which part can you use CPF to pay?

If the remaining lease of your dream flat can cover the youngest buyer until at least the age of 95, you will be able to utilise your entire CPF monies in the Ordinary Account to pay for the property up till the Valuation Limit.

Otherwise, if the years remaining on the lease will not cover the youngest buyer until they reach 95 years of age, you may want to use the formula below to calculate the maximum pro-rated amount of CPF savings you can use:

Pro-Rated CPF Usage = (Remaining lease of property – 20) / (95 - age of youngest buyer using CPF – 20)

Note: You are welcome to use our CPF Housing Usage Calculator if you want to determine how much money you can use to buy your second or additional property.

Click to Access CPF Housing Usage Calculator

Here is a list of HDB-related fees that you can pay with your CPF Ordinary Account:

- Initial payment in whole or in part (depending on whether you’re taking a HDB long or bank loan)

- Partial or full payment for the flat purchase

- Monthly mortgage instalments

- Legal fees (Depending on the law firm)

- Buyer's Stamp Duty and Additional Buyer's Stamp Duty (for Singapore PRs)

What are the Grants available for purchasing HDB Resale Flat?

While resale flats may be considerably more expensive than BTO flats, an upside to getting a resale flat would be being eligible for more grants from the government.

For BTOs, you will only be able to apply for the Enhanced Housing Grant (EHG). However for those of you buying a resale flat, there are two more grants available: the CPF Housing Grant and the Proximity Housing Grant.

Here’s how much you will be getting from the different grants:

|

Grant type |

How much you get |

Eligibility Criteria |

|

CPF Housing Grant (Family) |

First timers: $80,000 (SC/SC), $70,000 (SC/SPR) for 2-4 room resale, and $50,000 (SC/SC), $40,000 (SC/SPR) for 5 room or bigger First-timer and second-timer: $40,000for 2-4 room resale, and $25,000 for 5 room or bigger |

Married/engaged couples, 1st-time applicants can go with CPF Housing Grant Your average gross monthly household income must not exceed: ^S$14,000 ^S$21,000 if purchasing with extended family |

|

Enhanced Housing Grant |

Household Income, Grants Available up to $120,000 (for families), and $60,000 (for singles), depending on household income. CPF Enhanced Housing Grant |

Lower to upper – middle income applicants Flat lease 20 years or more. Flat must have sufficient lease to cover the youngest buyer and spouse/ fiancé to the age of 95 to qualify for the full EHG. Otherwise, the EHG will be pro-rated. |

|

Proximity Grant |

To live with parents: Singles – $15,000 To live near parents (within 4km): Families – $20,000 Singles – $10,000 |

|

Refer to our article CPF Housing Grants – How Much Can You Get When Buying an Resale HDB Flat? for more details on CPF Housing Grants available.

3. Gather More Information About Properties in Your Preferred Areas

Maybe you’ve already selected the area you’d like to purchase your house in. In such a case, we advise you to check out property prices in these preferred areas to stay on top of the game:

- Search for prices of recently sold HDB flats – It’ll help you know the prevailing prices of units in your preferred estate. You can use the official HDB website or the HDB map service to assist your search.

- Search for active listings on real estate portals like 99.co or PropertyGuru.com.sg – Do note that the prices here are marked up considerably since the sellers expect interested buyers to negotiate them down.

- Consult a real estate agent to obtain a Comparative Market Analysis (CMA) – A CMA offers you a highly accurate and free price estimate after a thorough analysis of current listings, past transactions, removed listings, and other important information.

- Use the Free Property Valuation tool from our website to obtain accurate estimates of property values – Similar to the CMA, using these tools allows you to get an accurate property value estimate, thus ensuring that the property you’re eyeing isn’t overpriced.

Don’t forget to check the SPR and ethnic quotas of the housing blocks as well. HDB website has a useful tool that allows you to check this information.

If the resale flat is within 4 kilometers of your children/parents, you can also apply for the Proximity Housing Grant. The Distance Enquiry Tool is a great resource to help you determine whether you can take advantage of this subsidy.

4. Choose Whether to Engage A Real Estate Agent or Do Everything On Your Own

While it’s not mandatory to hire a real estate agent, they are pretty helpful with certain things like:

- Negotiating with sellers to bring down the price

- Checking the property unit condition potentially expensive defects

- Conducting comprehensive background checks on the seller/property

- Obtaining a CMA on your shortlisted properties, ensuring you don’t overpay for the units

- Evaluating your financial condition to understand how much you can afford to spend on your house

- Uncovering any hidden real estate gems

But if you’re completely confident of your ability to handle any hidden surprises and other legal formalities, you can do everything on your own. The market rate for HDB Resale Buyer’s agent is 1% of the purchase price. To put things into perspective, that’s S$5,000 on a $500K flat.

5. Visit Prospective Homes

It’s important to pay close attention to every detail during this phase. During your house viewings, check out the amount of space the house has. Do look into nearby amenities and facilities as well. Your goal is to understand how liveable the units are and which home is the best for your needs. Ensure that the home faces the right direction (a Southeast-facing home unit receives refreshing sunlight in the morning while also being shielded from the afternoon heat). Make sure that it’s a well-maintained flat that doesn’t have any loan sharks after it. Don’t forget to schedule your house viewing in the afternoons as well. This allows you to check overall noise levels in the area and ensure that the heat isn’t too high during the day.

Watching out for these tiny details can help you save a fortune later on in renovation costs:

- Oddly shaped rooms/corners where your furniture might not fit properly

- ‘Bloodstained’ or rust-colored stains on the wall could imply the presence of bedbugs.

- Poor toilet flushing could indicate clogging in the drains.

- Termite-ridden or rotten wood could be a sign of future damage to doorframes, flooring, and furniture.

- Wet flooring patches indicate leaky pipes

- Peeling paint indicates water seepage

- Damaged flooring or tiles could cost you a fortune to repair later on – stay away as far as possible

- Built-in furniture, which needs to be replaced.

Don’t hesitate to look around the house around every corner. It’s always better to be safe than sorry. A single mistake here could wind up with you shelling out thousands in repairs, something you could have easily avoided with some extra diligence.

6. Get an Option to Purchase (OTP)

Have you found something that finally speaks to your mind? Excellent! Armed with your HFE letter, obtain an Option to Purchase from the flat’s seller as soon as possible. Do note that an AIP’s validity only lasts for 2 – 4 weeks whereas an HLE letter lasts for six months.The OTP will require Option fee, which will be set by the flat’s seller. It typically ranges between $1 - $1000, and typically the market practice is S$1,000. Do note that it’s fine to back out of the sale after the OTP is obtained. If you’re looking to lock down on the house but wish to make a final, thorough examination, an OTP will help you get extra time.

7. Submit A Request for Valuation

At this point, you’ve got 21 days for confirming your purchase. This period is meant to be used for arranging your finances and obtaining the loan required for funding the purchase. An HLE letter is sufficient if you’re financing the purchase with an HDB loan. A Letter of Offer is sufficient if you’re financing the purchase with a bank home loan. Whether it’s an HDB loan or a bank loan, you’ll have to request the loan institution for property valuation so that they can get started on their internal processes. This request needs to be filed on the working day right after the OTP’s Option Date – you cannot afford to lose any time here! The Request for valuation also requires you to pay a $120 non-refundable processing fee.

If you’ve already followed the steps mentioned above and researched property valuations in the area, you’re unlikely to be caught off-guard by the official valuation. It’s important for the actual price to be either below or equal to the property valuation – if the former is more than the latter, you’ll need to settle the difference in cash.

8. Exercise Your Option

If you are not taking HDB loan i.e. taking loan from banks, you need to first accept Letter of Offer from the bank before you exercise the OTP. When exercising the OTP, you’ll be required to pay the Option Exercise Fee upon doing so. This amount is usually S$4,000 and the total amount of Option Exercise Fee + Option Fee HDB shouldn’t exceed S$5,000 in all cases. This amount will be treated as your official flat deposit.

9. Submit Your Flat Resale Application

The next step involving filing the paperwork with the HDB. Log in with your credentials on the HDB Flat Portal. Proceed to submit your Resale Application online. The seller of the HDB flat will also be required to submit the Resale Application via their own accounts. These resale submissions need to be completed within seven days, else you risk cancellation of the application and forfeiture of the admin HDB fees, which typically ranges between $40 - $80.

The following details need to be submitted:

- The address of the flat

- Information regarding the OTP

- Particulars of the seller

- Your particulars and the particulars of your co-applicants

- Manner of holding (whether tenancy-in-common or joint tenancy, etc.) Click here to learn the difference between the joint tenancy and tenancy-in-common

- Information regarding the housing grants you’ve applied for

- Whether you’ve engaged any private lawyers or HDB solicitors

- The institution that approved your home loan.

The Seller may require more time to vacate the flat beyond the completion date, so-called Temporary Extension of Stay in HDB terms, and this will be discussed together with you before you pay for the option fee. Both parties will work on details such as who pay for the Town Council fee, Property Tax, utility bills, etc. Generally the Seller will pay for all up to the date of vacating the flat. This arrangement is done privately, and real estate agents should prepare an agreement to prevent future dispute and misunderstanding. Both parties must indicate on HDB Resale Submission if there is Temporary Extension of Stay.

10. Endorse the Resale Documents and Pay Applicable HDB Legal Fees

After the HDB has accepted your resale application, the paperwork will be reviewed thoroughly to ensure everything’s in order. You’ll be sent an SMS from HDB within six days, requesting you to open the Flat Portal for endorsing the documents. You will also need to book an appointment with the institution that approved your home loan (your bank or HDB). During this appointment, you can formalize the loan terms and gather more details regarding any grants you’re applying for to finance the purchase.

11. Carry out A Flat Inspection

You’re almost done by this point. All that’s left is for the seller and HDB to sign off on the deal. Next, HDB will get some of their technical execs to carry out a thorough inspection of your resale flat, in order to ensure that no illegal alterations have been made to the flat by the seller. However, that’s the extent of their inspection duties. It is your responsibility to inspect the flat for damages or structural troubles. HDB is not responsible for certifying the flat’s condition at any stage – that’s on you. Once the seller has moved out, carry out another flat inspection to ensure that it is vacant. You can consult the valuation report and make sure that everything is still intact without any damage.

12. Attend the Flat Resale Completion Appointment

We’re almost done! The last step is to attend the Flat Resale Completion Appointment, which will be held at the HDB hub if you’ve engaged the HDB’s solicitor. You’ll need to have printed copies of the payment advice, which can be obtained from the official HDB Flat Portal – these documents will help you pay the remaining balance on your flat. We advise you to get there early and visit the Payment Office (located on Level 3 of the Hub) for settling the bill. You should also buy HDB Fire Insurance if you’re financing the purchase with an HDB loan. You can meet up with the Customer Relations Manager after that to complete signing the appropriate documents, after which you’ll be issued a letter of confirmation as proof of the lease agreement transfer and given the keys to the flat. In case you have a private lawyer to represent you at this appointment, your solicitor’s presence and action on your behalf is equally valid. That’s it!

To make sure you get to live in your dream home, click on Contact Pinnacle button below, and we’ll be in touch with you in a minute.

Our Key Executive Officer (KEO) holds BSc. (Real Estate) Hons. from the National University of Singapore (NUS) and achieved SEAA Gold awards in 2021 & 2022, the only national-level awards recognised by the Council for Estate Agencies (CEA), and holds more than 10 years of experience.

At Pinnacle Estate Agency, we strongly believe in sharing our real estate knowledge to the public. For more content like this article, check out our Singapore Property Guides.